How to Track Customer Credit (Deni) and Reduce Bad Debt in Kenya

Struggling with unpaid customer credit in your duka? Learn proven strategies to track deni, set credit limits, and reduce bad debt for Kenyan small businesses.

The Deni Problem Every Duka Owner Knows

If you run a duka in Kenya, you know deni (customer credit) all too well. A regular customer asks to take sugar and pay on Friday. Another neighbour needs cooking oil until payday. Before you know it, you have KES 30,000 or more sitting in unpaid credit — money that should be in your pocket or reinvested in stock.

Deni is part of doing business in Kenya, especially in residential areas where customers are your neighbours and community members. Refusing credit entirely can cost you loyal customers. But giving credit without a system will slowly drain your business dry.

Why Deni Gets Out of Control

The typical duka credit system looks like this: the owner writes the customer's name and amount in a notebook. Maybe. Sometimes it is just memorized. When the customer comes to pay, there is a debate about the exact amount. Sound familiar?

Here is why this fails:

- No clear records — Handwritten entries get smudged, pages get torn, and notebooks get lost. You end up with incomplete records and no proof of what is owed.

- No credit limits — Without a cap on how much a customer can borrow, balances spiral. A customer who owes KES 500 today might owe KES 5,000 next month.

- Social pressure — It is hard to say no to a neighbour or a long-time customer. Without a policy, every request becomes an emotional decision.

- No follow-up system — When is payment due? Who should you remind today? Without a system, collections depend entirely on your memory.

- It affects your cash flow — Every shilling in deni is a shilling you cannot use to restock. High deni balances mean empty shelves and lost sales.

Setting Up a Deni Management System

1. Record Every Credit Transaction Immediately

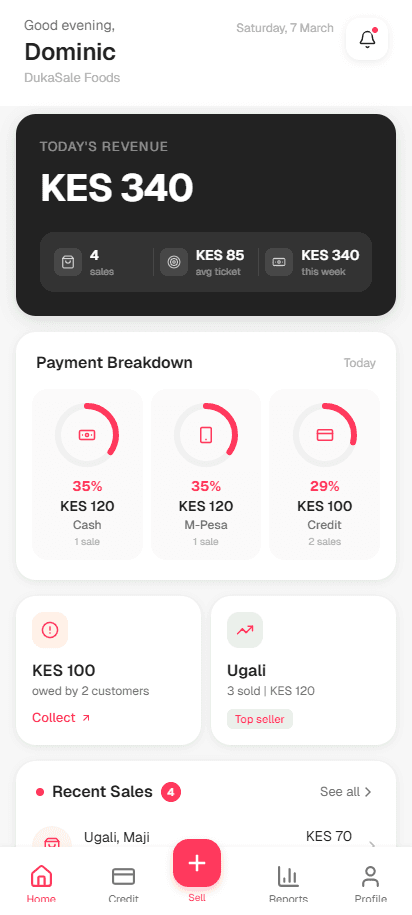

The moment you give credit, record it. Not later. Not at the end of the day. Right then. Include the customer name, items taken, total amount, and the date. If you use an app like DukaSale, this is as simple as completing a sale and selecting "Deni" as the payment method.

2. Set Clear Credit Limits

Decide upfront how much credit each customer can have. This could be based on their payment history:

- New customers — No credit until they have been buying from you for at least a month with cash.

- Regular customers with good history — Credit limit of KES 1,000-2,000.

- Long-term trusted customers — Higher limits, but still capped. Nobody gets unlimited credit.

When a customer hits their limit, the system (or you) says no. This removes the emotional difficulty — it is the policy, not a personal rejection.

3. Set Payment Deadlines

Every credit transaction should have an expected payment date. "End of month" or "next Friday" — be specific. This creates accountability and gives you a basis for follow-up.

4. Follow Up Consistently

When a payment date passes, follow up immediately. A friendly reminder the next day is much more effective (and less awkward) than waiting two weeks. Many POS apps can show you which debts are overdue, making this easy to manage even with dozens of credit customers.

5. Record Partial Payments

Customers often pay in instalments. Make sure your system tracks partial payments so you always know the remaining balance. This prevents the "but I already paid some" disputes that plague paper-based systems.

How to Handle Difficult Deni Situations

The Customer Who Always Delays

Lower their credit limit. If they consistently pay late, reduce their limit until their behaviour improves. Eventually, move them to cash-only if the pattern continues.

The Customer Who Disputes the Amount

This is where digital records shine. With an app, you can show them an itemized list of every transaction — dates, items, amounts. There is no argument when the data is clear.

The Customer Who Never Pays

After multiple reminders and a reasonable waiting period, you have to accept the loss and cut off credit. Write it off as a business lesson. It is better to lose one customer than to keep supplying someone who never pays.

Using Technology to Manage Deni

Digital tools have transformed deni management for Kenyan dukas:

- Automatic balance tracking — The system calculates running balances for each customer. No manual addition.

- Customer profiles — See each customer's full credit history: when they borrowed, what they bought, when (or if) they paid.

- Overdue alerts — Know instantly which customers have passed their payment dates.

- Payment recording — Log payments easily and see the updated balance immediately.

- Reports — See your total deni exposure at a glance. Know if your credit situation is getting better or worse over time.

Protecting Your Business Cash Flow

The golden rule of deni: never let your total outstanding credit exceed 10-15% of your monthly revenue. If you sell KES 200,000 per month, your total deni should not exceed KES 20,000-30,000.

If you are already above that threshold, take these steps:

- Stop giving new credit until existing debts are collected.

- Prioritize collection from your largest debtors.

- Reduce credit limits across the board.

- Consider offering a small discount for cash payments to encourage customers to pay upfront.

The Bottom Line

Deni is not the enemy — unmanaged deni is. With clear policies, consistent record-keeping, and the right tools, you can offer credit as a competitive advantage without putting your business at risk. The key is to track every shilling, follow up promptly, and never let emotion override your credit policy.

Ready to try DukaSale?

Free POS app for Kenyan dukas. Track sales, inventory, M-Pesa payments, and customer credit — all offline.

Download Free